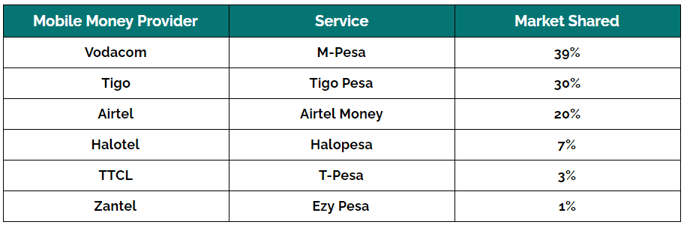

Sending and receiving money through mobile devices started in Tanzania back in 2008. Tanzania was one of Africa’s first countries (with Kenya) to launch mobile money services in Africa. With six mobile money services – Vodacom, Airtel, Tigo, Halotel, TTCL and Zantel – mobile money in Tanzania is a substantial contributor to growth and development in the region.

There are 16.5 million active mobile money users in Tanzania, transacting over $27 billion every year. Such a high adoption of mobile money accounts is led by a staggering growth in mobile users. Tanzania is home to 46.847 million mobile subscribers, which is around 78% of the total population.

Mobile money and SACCOs in Tanzania

Mobile money in Tanzania is changing how people make payments, especially in areas with limited or no access to formal banking. Moreover, the impact is not limited to payments but can also be seen in savings and loans through social saving groups called SACCOs.

SACCOs have become more mature, and their need for more sophisticated financial services has become more evident. They need to store huge amounts in savings, provide money as loans, and manage interests. These SACCOs, linked with mobile money accounts, can bring massive changes for their members. It can help them manage their operations in a faster and more efficient way. Let’s know more about how mobile money can bring transformative changes for SACCOs.

Better financial inclusion

Financial inclusion is probably one of the biggest challenges faced in Tanzania. According to the FSDT and the Bank of Tanzania report, “10.6 million Tanzanians use informal channels to access financial services.”

Mobile money can bring radical changes in the scenario by bridging the gap between formal financial services and the unbanked. Members can have mobile money wallets to contribute their deposits to their SACCOs. They can avail loans through wallets, and once approved, the loan amount can also be disbursed through the same channel. Similarly, they can repay their loan through mobile payments.

Banks and financial institutions can use the data to bring the unbanked population under the umbrella of formal financial services.

Digitization of the informal sector

The adoption of mobile money in Tanzaniacan open new ways to innovate and provide members with more digital solutions. For example, the transactional data of users can be used to analyze user preferences. Based on that, providers can offer relevant loan and saving schemes to the users.

Airtel Uganda partnered with Grameen Foundation and Plan Uganda to design and launch a mobile money product tailored to the needs of savings groups.

Wakandi is one of the companies that aims to accelerate digital transformation for SACCOs in Tanzania. We have built an app called the Credit Association Management System (CAMS) that SACCOs can use to manage their operations digitally. With CAMS, members can

-

Send contributions via mobile wallets

-

Apply for loans online and get the amount online

-

Manage loans and other records automatically

-

Maintain account books

You can read more about CAMS here.

We are all set to launch CAMS in Tanzania as we have successfully onboarded our first of many SACCOs from Dodoma. You can read more about the CAMS launch update.

Empower women and poor

Mobile money can help SACCOs to empower women and the poor through various means. For women, mobile money can offer accessibility to faster and secure payments, reduce the need for cash, and increase the availability of loans at a click of a button. For the poor, SACCOs can provide affordable means to save money and provide loans at a lower cost.

Conclusion

Mobile money is quickly emerging as a way to faster and more efficient payments. The technology will continue to be an important means of accelerating financial inclusion and innovation amongst SACCOs and the entire informal sector. Increasingly, it will also enable the development of newer digital solutions and bridge the unbanked to formal financial services.